U.S. Industrial Outlook: December 2016

Overview of the Forecast Picture

Every three months, the MAPI Foundation simulates the Global Insight U.S. macroeconometric model in order to generate a forecast of growth in the U.S. economy as well as its manufacturing sector and subsectors.

Our current five-year forecast is one of persistently sluggish activity. We expect no more than 2% annual growth in U.S. GDP through and including 2020. We predict less than 1% annual growth in U.S. manufacturing output for 2016 and 2017 and then growth of 1% or a little more through and including 2020.

Both manufacturing and the overall economy continue to be plagued by a host of factors. One is the risk aversion that has resulted in 16 years of malaise in capital equipment investment. In addition, structural impediments such as weakening labor productivity growth and the beginning of a period of population aging are constraining long-term growth potential.

Since manufacturing is the most globally connected of all U.S. sectors, its growth is particularly hurt by weakness and instabilities in the post-2009 world economic picture. In simulating the Global Insight model to produce the current forecast, we assume continued weakness in global economic performance. There is much evidence to support this assumption. While emerging market troubles, particularly in Brazil and Russia, appear to be reaching at least a temporary stasis, the stability of the trough is unclear, especially in light of the protracted slowdown in the globally influential Chinese economy.

Fears that the eurozone is a potential source of a globally destabilizing crisis have certainly abated, which is a boon to the efforts of emerging markets to stabilize. But eurozone growth remains frustratingly slow, and long-term uncertainties abound, particularly in the wake of the United Kingdom’s decision to relinquish its 43-year membership in the European Union. The tactical and logistical uncertainties in the post-Brexit years could by themselves, apart from any market or policy realities, put a cap on growth.

After a weak first half of 2016, U.S. economic growth has clearly accelerated. But it is a strangely bifurcated picture, with strength coming from the consumer and improved export demand; equipment investment, meanwhile, has suffered four consecutive quarterly contractions. Consequently, from the perspective of industrial manufacturers, U.S. GDP growth has been deceptive in that the benefits of growth are realized more outside of the manufacturing sector. Weakness in business fixed investment is now a long-term problem that has hurt manufacturing performance and contributed to a moribund productivity picture, with negative consequences for potential U.S. growth.

MAPI Foundation Forecast of U.S. Economic and Manufacturing Growth

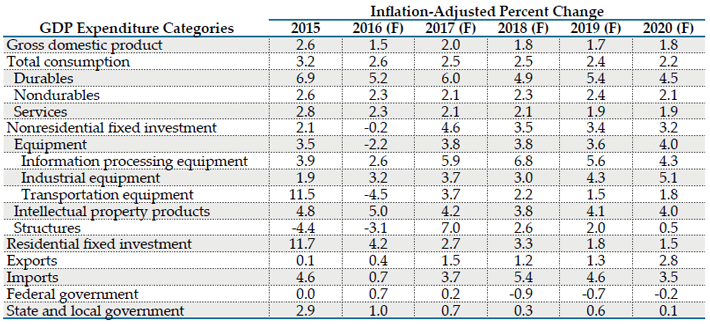

Table 1 shows the MAPI Foundation’s current prediction for growth in U.S. GDP and key components of GDP through 2020. Relative to historic norms, growth is expected to remain sluggish throughout the forecast period, achieving only 2% in 2017. Structural and long-term trends are reflected in this weak outlook, including poor productivity performance in the U.S. and key parts of the world, the realities of an aging population in the coming years, stubborn global economic weakness, and a high dollar as the U.S. remains, in spite of muted performance, the relatively strong economic player among its trading partners.

Table 1 – MAPI Foundation Forecast of U.S. Growth of GDP and Components

F=Forecast

Source(s): MAPI Foundation, November 2016

While moderate to weak consumer spending growth is expected, equipment investment activity will likely continue to be a drag on economic and manufacturing performance. After an expected 2.2% contraction during 2016, annual growth of equipment expenditures is expected to average 3.8% for the balance of the forecast period. This is a remarkably weak showing for an indicator that has often achieved double-digit growth rates. The weakness in equipment investment, now a 16-year phenomenon, has been one of the biggest demand-side challenges for U.S. manufacturers, frustratingly negating the benefits of what has been a relatively competitive position in global machinery markets.

Weak global demand results in a weak export forecast, with annual export growth expected to not accelerate above 2% until 2020. The simple reality is that export growth has weakened significantly since 2010 and looks to remain weak for the intermediate term.

Given that equipment investment demand and export demand are crucial to manufacturing performance, it is not surprising that the U.S. manufacturing forecast, as shown in Table 2, is quite weak. After essentially flat growth in 2016, manufacturing growth is expected to be less than 1% during 2017 and then remain at or just above 1% through and including 2020.

Table 2 – MAPI Foundation Forecast of U.S. Manufacturing Output Growth

F=Forecast

Source(s): MAPI Foundation, November 2016

Forecast of Major Manufacturing Subsectors

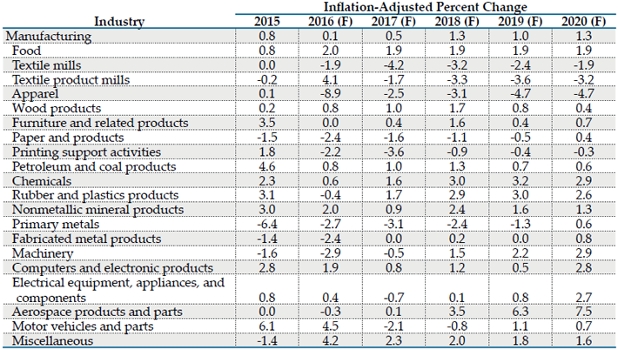

Table 3 shows the five-year outlook for manufacturing subsectors. Amidst a generally weak picture, the relatively strong performers are expected to be food, petroleum, chemicals, rubber and plastics, and nonmetallic mineral products. Moderate but steady consumer spending is likely supportive of positive performance in this group of subsectors.

Table 3 – MAPI Foundation Forecast of U.S. Manufacturing Industry Output Growth

F=Forecast

Source(s): MAPI Foundation, November 2016

Miscellaneous manufacturing also has a relatively strong outlook. It is composed in part by medical equipment, a growth industry benefiting from an aging population, and some specialized consumer products such as sports equipment.

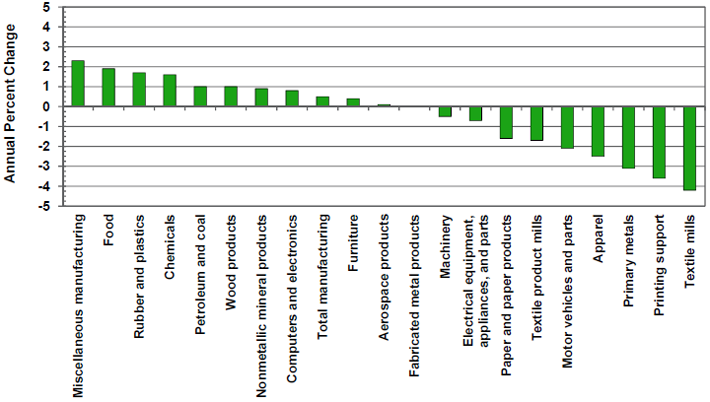

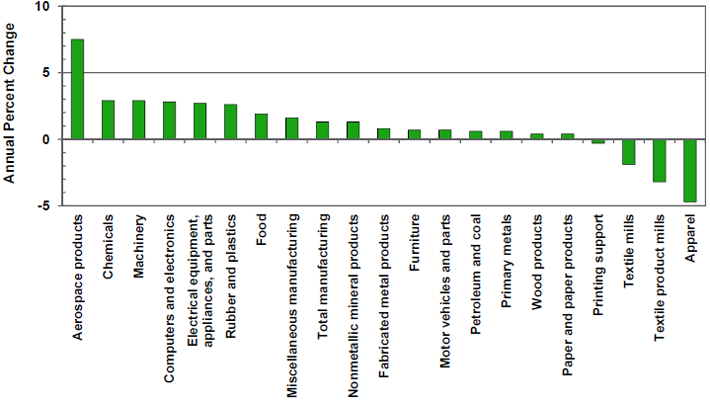

Figures 1 and 2 show the lineup of industry forecasts for 2017, the first full year of the forecast, and 2020, the last year of the forecast period. While food, rubber and plastics, and chemicals are among the strong performers during 2017, aerospace products and parts is predicted to be the dominant growth subsector during 2020. The expectation of sustained strength in air travel demand creates a favorable outlook for the most globally competitive of U.S. manufacturing subsectors, particularly in 2019 and 2020; aerospace enjoyed an $81 billion trade surplus in 2015. A measure of long-term risk might be entering the aerospace picture, however, as the U.S. share of global aerospace exports has been flat since 2009.

Figure 1 – MAPI Foundation 2017 Forecast of Output Growth in Manufacturing Industries

Source(s): MAPI Foundation, November 2016

Figure 2 – MAPI Foundation 2020 Forecast of Output Growth in Manufacturing Industries

Source(s): MAPI Foundation, November 2016

As manufacturing growth shows very moderate but persistent improvement, the machinery subsector will likely join the growth leaders in 2020, since machinery demand tends to correlate with overall manufacturing performance. But there are risks in this forecast given the potential for significant increases in the cost of capital as interest rates rise and for the persistence of a high dollar. Further, the very nature of the equipment investment problem has been one of risk-aversion psychology, which can be difficult to quantify and thus to forecast.

Outlook Perspective: Consumer, Investment, and Materials-Related Industries

For further perspective, Tables 4, 5, and 6 segment detailed industry forecasts into consumer-related, investment-related, and materials-related manufacturing, respectively.

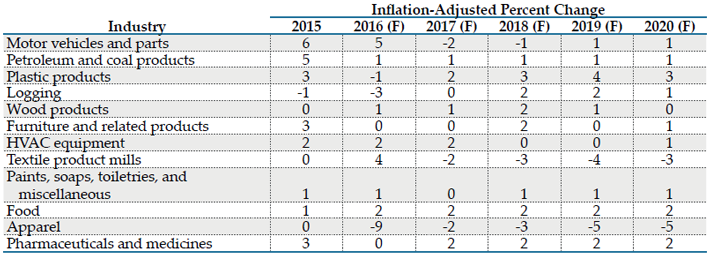

Table 4 – MAPI Foundation Forecast of Output Growth in Consumer-Related Industries

F=Forecast

Source(s): MAPI Foundation, November 2016

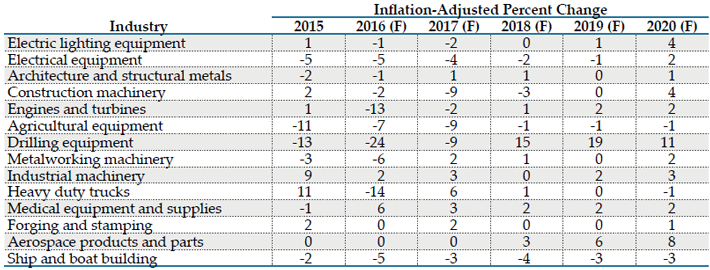

Table 5 – MAPI Foundation Forecast of Output Growth in Investment-Related Industries

F=Forecast

Source(s): MAPI Foundation, November 2016

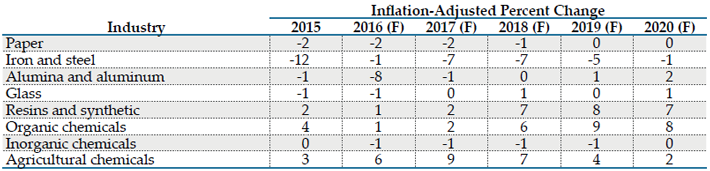

Table 6 – MAPI Foundation Forecast of Output Growth in Materials-Related Industries

F=Forecast

Source(s): MAPI Foundation, November 2016

Apart from textile product mills and apparel—both industry sectors in long-term decline in the U.S.—the consumer-related manufacturing growth outlook is positive if not strong, a mirror of our moderate consumer spending forecast.

By contrast, investment-related manufacturing is weaker and more volatile. Expected volatility in drilling equipment output is partially a response to a dramatic oil price cycle, while the generally sluggish outlook for total manufacturing growth is reflected in the muted but positive outlook for output gains in industrial machinery and metalworking machinery.

Materials production forecasts reflect the still weak but somewhat stabilizing global commodities outlook. Steel gluts and the slow manufacturing outlook are behind our forecast for iron and steel output contraction through 2020.

Forecast Issues and Forecast Risks

The most significant of the “known unknowns” in the MAPI Foundation’s current U.S. manufacturing forecast is the possibility that the new U.S. Congress will enact tax and regulatory reform and engage in considerable infrastructure spending. Such measures place an upside risk to the outlook.

Other forecast issues include the progress of Brexit as it affects UK and eurozone growth and the potential for upside risk on the outlook for U.S. and global interest rates. A further increase in the already high dollar is also a forecast risk. Upside surprises in interest rates and the dollar could somewhat neutralize the positive impacts of growth-enhancing policies in the U.S.

Looking Ahead

While at the moment, the U.S. economic and manufacturing growth outlook is sluggish, growing questions about a multitude of turning points in the U.S. and global economic pictures will shape the MAPI Foundation’s manufacturing forecast in the coming quarters. Analysts are carefully watching for shifts in global interest rates as markets price in possible changes in central bank policies. Questions over whether the Chinese economy is reaching a bottom in its protracted slowdown and whether U.S. growth is really accelerating will continue into the new year. The MAPI Foundation will be monitoring these trends and potential policy changes and incorporating them into our modeling activities.