Myth-Busting American Manufacturing

The MAPI Foundation wants to set the record straight. U.S. manufacturing is a vibrant industry.

Disparaging myths have circulated about American manufacturing for decades. Parents have discouraged their children from going into a manufacturing career because they think factories are “dirty and dangerous,” or lacking a solid wage and career opportunities. Manufacturers in other countries−such as Germany and Japan−are perceived as far more innovative than their U.S. counterparts. And, the most virulent rumor of all, people believe that manufacturing has vanished from the United States. When was the last time you heard, “We don’t make anything here anymore”?

The prevalence and endurance of these misperceptions have serious ramifications for the manufacturing industry. When schoolchildren believe manufacturing is not a sound career choice, they will not consider a job in that sector. When economists and policymakers call manufacturing irrelevant in today’s economy, they continue to perpetuate myths that harm the sector.

This study debunks these myths. Over the years, many experts have tried to dispel falsehoods and have offered detailed arguments about manufacturing’s key role in raising living standards. MAPI Foundation’s research has found that manufacturing’s role in prosperity is much bigger than national statistics suggest; the value added from the entire manufacturing value chain is roughly 1/3 of both GDP and employment.

With a new administration and Congress in the nation’s capital and a renewed spirit to build a more vibrant manufacturing sector, it’s time to set the record straight. By truly understanding manufacturing, we can rebuild the factory sector’s standing among educators, parents, and policymakers. We can support better job opportunities and consistent economic growth for future generations.

Read on for a nonpartisan, rhetoric-free understanding of manufacturing in America.

Myth No. 1: U.S. Manufacturing is in Decline

There is often a common misperception of a bleak picture for the U.S. manufacturing sector. With political rhetoric on both sides of the aisle, it is understandable that many Americans may think that the factory sector is in serious trouble and nothing is made inside U.S. borders anymore, leading to a decline in global competitiveness, and massive job losses at home.

Being the most globally exposed segment of the U.S. economy, manufacturing is naturally going to have a world of challenges. But there is also a world of promise. Using manufacturing dynamics, globalization, and economics, we’ll prove that manufacturing decline is only a myth.

Strong Goods Production Within U.S. Borders

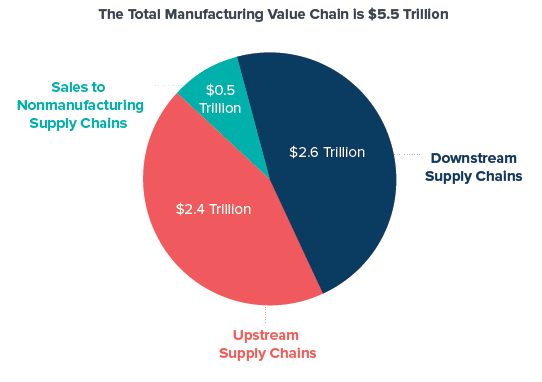

The United States remains a major force in global manufacturing. If the U.S. manufacturing sector were its own economy, it would be the seventh largest in the world, with $2.2 trillion of value added in 2015. This value is greater than the economic output of India, Italy, Brazil, and Canada. Moreover, a 2016 MAPI Foundation report found that by some estimates, the total manufacturing value chain could be as high as $5.5 trillion, or about one-third of the U.S. economy. i U.S. manufacturers also produce intermediate inputs for other companies across sectors, both domestic and abroad.

U.S. Manufacturing is Globally Competitive

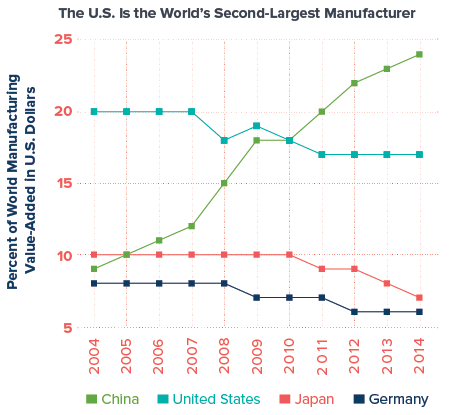

The U.S. is the second largest manufacturer in the world and is responsible for 17% of world manufacturing activity.

Many incorrectly equate the rise of Chinese manufacturing with a decline in U.S. manufacturing. It is true that China took the top spot as the world’s largest manufacturer in 2010. However, considering that China is a lower wage country with a population more than four times that of the U.S., this is not surprising. China’s share of global manufacturing rose from 9% in 2004 to 24% in 2014. ii

The U.S. sector’s domestic value increasingly comes from advanced manufacturing, which leverages the growing availability of cutting-edge design, production, and automation technologies to create fundamental efficiencies in the production of a wide range of goods. Such efficiencies in production have contributed to success in global markets, and have allowed the U.S. to be the third largest manufacturing exporter.

Further testifying to U.S. global competitiveness, foreign corporations heavily invest in American industry. Foreign multinationals held a bit over $1.2 trillion of investments in U.S. manufacturing in 2015.

Sources: MAPI Foundation and INFORUM

Global Forces Cause Both Job Loss and Job Gain

Manufacturing employment is complex — and arguably, the most misunderstood of all aspects of manufacturing. There is no denying that the U.S. factory sector has become less of a job creator over time. Between 2000 and 2010 the factory sector shed 5.7 million jobs. But even after such a steep loss, manufacturing still employs nearly 9% of the U.S. workforce. As a MAPI Foundation study shows, for each full-time equivalent job in manufacturing dedicated to producing value for final demand, there are 3.4 full-time equivalent jobs created in nonmanufacturing industries.iii

Offshoring is most often the first thing blamed for any manufacturing employment stress. Other factors, however, seem to account for a greater share of the decline in U.S. manufacturing employment over the past several decades. According to McKinsey & Company, trade and outsourcing are responsible for just 20% of the jobs shed by the U.S. factory sector during 2000-2010, with much of the remainder a result of productivity growth.iv

Further, in an integrated global economic system the U.S. does not merely lose jobs to location decisions, it gains jobs. The number of U.S.-based jobs at foreign-owned manufacturers has been steadily rising following the 2008-2009 recession.

Employment at these foreign-owned manufacturers reached 2.4 million in 2014. In that year, this constituted approximately 20% of all domestic U.S. manufacturing jobs. Foreign manufacturers are attracted to U.S. advantages such as new market opportunities, proximity to existing customers, and business disruption risk.v

Sources: United Nations and MAPI Foundation

Myth No. 2: Manufacturing is a Poor Career Choice

A manufacturing career offers ambitious, talented people a great many rewards. As an increasingly global segment of the U.S. economy, there is the promise of an international aspect to a manufacturing career. Science, technology, engineering, and mathematics (STEM) are all critical elements of the manufacturing world, offering a chance to be on the cutting edge. The range of the factory sector is such that good opportunities exist even for those without a 4-year degree. Many people may be surprised to learn that manufacturing is notable for its relatively low turnover and lengthy job tenure, making it a stable career choice in a difficult economic environment.

As with many things in the manufacturing world, reality can be clouded by perceptions rooted in stereotype rather than fact. A 2015 study by The Manufacturing Institute and Deloitte revealed that only 37% of Americans would recommend that their child seek a career in manufacturing.vi For the sake of a needed manufacturing workforce, and for the benefits of those who are failing to seek potentially rewarding manufacturing careers, this perception needs to change.

Global Forces Cause Both Job Loss and Job Gain

Manufacturing employment is complex — and arguably, the most misunderstood of all aspects of manufacturing. There is no denying that the U.S. factory sector has become less of a job creator over time. Between 2000 and 2010 the factory sector shed 5.7 million jobs. But even after such a steep loss, manufacturing still employs nearly 9% of the U.S. workforce. As a MAPI Foundation study shows, for each full-time equivalent job in manufacturing dedicated to producing value for final demand, there are 3.4 full-time equivalent jobs created in nonmanufacturing industries. iii

Offshoring is most often the first thing blamed for any manufacturing employment stress. Other factors, however, seem to account for a greater share of the decline in U.S. manufacturing employment over the past several decades. According to McKinsey & Company, trade and outsourcing are responsible for just 20% of the jobs shed by the U.S. factory sector during 2000-2010, with much of the remainder a result of productivity growth iv Further, in an integrated global economic system the U.S. does not merely lose jobs to location decisions, it gains jobs. The number of U.S.-based jobs at foreign-owned manufacturers has been steadily rising following the 2008-2009 recession.

Employment at these foreign-owned manufacturers reached 2.4 million in 2014. In that year, this constituted approximately 20% of all domestic U.S. manufacturing jobs. Foreign manufacturers are attracted to U.S. advantages such as new market opportunities, proximity to existing customers, and business disruption risk.v For the sake of a needed manufacturing workforce, and for the benefits of those who are failing to seek potentially rewarding manufacturing careers, this perception needs to change.

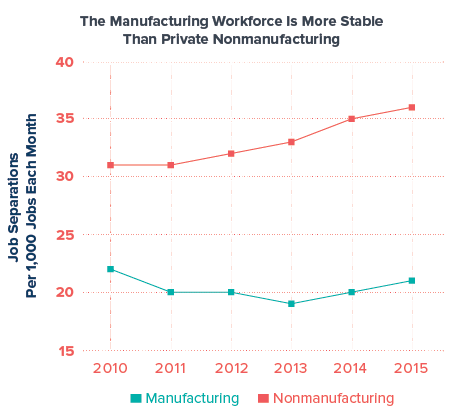

U.S. Manufacturing Offers Stable Careers

There is evidence that a manufacturing job is more stable than the average nonmanufacturing private sector job. The manufacturing sector has a lower rate of job turnover than jobs in nonmanufacturing.vii In addition, the separation rate is consistently much lower in manufacturing, and the sizable gap has grown since 2010. In 2015, 36 workers per thousand nonmanufacturing jobs separated each month. A substantially lower 21 workers per thousand jobs separated from manufacturing establishments.

Manufacturing workers consistently have a much higher tenure with current employers than private sector nonmanufacturing employees on average. According to the U.S. Department of Labor’s job tenure data (collected every two years), the median employed manufacturing worker had 5.3 years of tenure with their employer in January 2016 compared with only 3.7 years for the overall private sector.viii How does a manufacturing paycheck compare to compensation for other sectors? Government data on the employer cost of employee compensation in major sectors of the economy show that during the first half of 2016 wages and salaries in manufacturing were 16% higher than in service-providing industries.ix

Just as important, manufacturers appear to provide a more generous benefit payout than non-manufacturers. During the first half of 2016, manufacturers provided 65% more in benefits per hour of employee work than employers in the service industry.

Workers in virtually all occupations, reflecting a wide variety of skills and educational attainment, earn more in manufacturing than outside of manufacturing.

Sources: U.S. Bureau of Labor Statistics and MAPI Foundation

U.S. Manufacturing Employs Highly Educated Workers

Will those with a high level of education feel rewarded in a manufacturing career? The educational attainment of the manufacturing workforce is better than is often assumed, although there is some complexity in the picture. Since production workers make up more than half of the manufacturing workforce, a disproportionately large share relative to the general economy, manufacturing has a lower college degree ratio, as a four-year degree is not often necessary for production positions. Conversely, a disproportionate share of STEM-based work takes place in manufacturing.

The sector employs 37% of the U.S. economy’s architecture and engineering workers and 16% of all life, physical, and social scientists.x

Sources: National Science Foundation, Business R&D and Innovation Survey

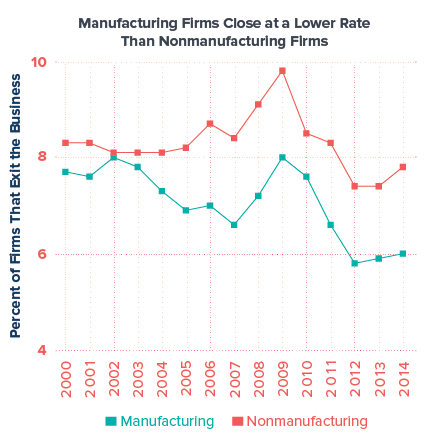

Manufacturing Startups are Less Risky

What about a manufacturing career for those who dream of owning their own business? Opening any new business is risky, but there is evidence that manufacturing entrepreneurship entails below-average risk. Relative to other types of firms, manufacturing companies have a lower closure rate; this holds true across the span of company ages, not just those companies that began within the last few years.

The U.S. government tracks every firm in the United States that has at least one employee and provides data on longevity by sector. In 2014, 23% of nonmanufacturing firms with one full year of operations closed compared with 20% of manufacturing firms. Manufacturing comes out modestly ahead across all other company age cohorts measured by the Department of Labor. Businesses with at least 26 years of operations had a 5% closure rate in nonmanufacturing versus

4% in manufacturing.

In 2000, the nonmanufacturing firm closure rate across all age groups was 8.4% compared to 7.7% for manufacturing. In 2014 the closure rates was 7.8% for nonmanufacturing and 6% for manufacturing.

Sources: National Science Foundation, Business R&D and Innovation Survey

Manufacturing Entrepreneurship is Successful

Given the relatively lower risk of closure, the lesser start-up rate in manufacturing is puzzling. Entrepreneurial activity outside of the manufacturing sector is more vibrant, although overall business start-up activity has weakened in general.

In 2014, the startup rate was 8.2% in nonmanufacturing and only 4.2% in manufacturing. This entrepreneurial gap has been persistent. Since 2002, the startup rate difference between manufacturing and nonmanufacturing has averaged 3.9 percentage points.xi

With positive signs on job stability, compensation, paths for educated workers, and entrepreneurship, a change in perception could be the trigger that motivates career interest in the factory sector and thus provides the U.S. with the manufacturing workforce that it has long needed.

Myth No. 3: U.S. Manufacturing Isn't Needed

Manufacturing provides an important engine for economic growth in developing countries but remains a critical force in advanced economies as well. The domestic factory sector in the U.S. ensures that the country is not solely dependent on foreign goods producers to meet the 70% of the economy that is consumer spending.

Dependence on foreign goods production would also have a negative consequence to responsiveness for evolving U.S. customer needs. The U.S. economic system is diverse and experiencing rapid changes in age and spatial demographics. Responsiveness to structural change is key to an economically vibrant supply of goods. This best comes from having a growing manufacturing sector within U.S. borders. The need for responsiveness over the long-term gives rise to the need for innovation, an element of competitiveness for any country. In the U.S., the manufacturing sector is the strongest source of innovation investment and output.

Without Manufacturing, the U.S. Would Not Realize the Considerable Gains from Trade

Although trade is currently under political fire, economists agree that it increases the wealth of a nation. A competitive domestic manufacturing sector is the best way to leverage the wealth-generating potential that lies beyond our borders. Economic strength and innovative progress require that America, whose population is approximately 5% of the global population, fully engage with the other 95% of the world. Without a domestic manufacturing base, the U.S. economy would have a significantly diminished presence in global export markets, of which goods exports account for between 65% and 70%.

The services sector alone cannot pay for all of the goods that businesses and consumers want to purchase. Without the funds generated from the export of goods, the U.S. would need to increase domestic savings massively or persuade foreign investors to finance a $2 trillion deficit to cover the current level of goods imports.

The services trade surplus is a drop in the bucket compared to the magnitude of goods imports. Quite simply, the U.S. needs to make and sell goods in foreign markets to be able to afford to import the goods to satisfy U.S. consumer demand.

Domestic U.S. manufacturing is not just important to the U.S. It contributes to global economic stability as well. Multi-country supply networks are becoming the backbone of global goods production. Innovation is happening at such a quick pace that the production of increasingly research and development (R&D)-intensive capital goods cannot be done efficiently in only one country. The absence of the U.S. from these networks would diminish global manufacturing strength, to the detriment of global stability, and ultimately U.S. economic stability.

Without Manufacturing, the U.S. Would Lack Innovation

In decades of research, economists have come to understand that innovation-generating activity matters for business competitiveness, economic growth, and living standards. With the unfortunate stereotypical view of the U.S. manufacturing work environment as being dark, dirty, and dangerous, it is hardly surprising that many view the factory sector as old-fashioned and unimaginative. Nothing could be further from the truth. By many accepted metrics, U.S. manufacturing is a powerhouse of innovation.

Sources: U.S. Bureau of Economic Analysis and MAPI Foundation

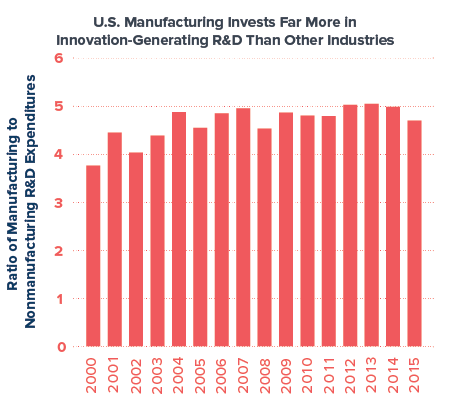

It is easy to visualize the contribution of innovation from manufacturing. One only has to consider the power of the computer revolution and the preponderance of a range of new manufacturing process technologies. From additive manufacturing to the Internet of Things, to advanced robotics, it’s easy to see the effects of innovation well beyond specific industries, and beyond the manufacturing sector itself. Computers have fundamentally changed the workplace for everyone. Robotics, artificial intelligence, and 3D printing may do the same.

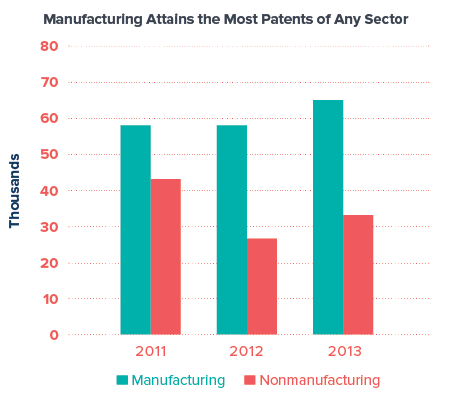

Data certainly confirm this view of the manufacturing sector as being a powerful innovation generator. Two accepted metrics, 1) R&D spending on the input side, and, 2) patents on the output side, tell the story. R&D is not, by any means, a complete measure of innovation investment. But, it arguably demonstrates a company’s commitment to a strong innovation outcome. Nonetheless, patent growth correlates to innovation. Manufacturing R&D investment has been 4 to 5 times greater than nonmanufacturing R&D.

With dominance in R&D and patents, the manufacturing contribution to future economic growth and competitiveness is clear. At an active time of manufacturing policy consideration, it is important for the public, business leaders, and policymakers, to move away from the stereotypical view of outdated manufacturing and see the light of innovation generation that comes from manufacturing companies.

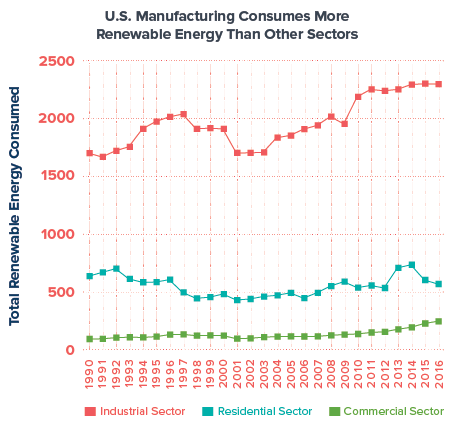

Myth No. 4: Manufacturing is Unduly Harmful to the Environment

The commonplace picture of U.S. manufacturing as a smokestack industry underlies a longstanding concern about the environmental damage that can arise from manufacturing processes. In reality, manufacturing profitability and environmental outcomes aren’t mutually exclusive.

Market Incentives Support Environmental Stewardship

Regulations and new technologies have made a difference to the environmental footprint of the U.S. factory sector. Further, public-private partnership efforts have proven to be wise investments. Such programs include Building Better Plants, a U.S. Department of Energy program that collaborates with leading manufacturers and water utilities to improve energy efficiency and competitiveness. Other effective programs include the Environmental Defense Fund and the Carbon Disclosure Project, the latter producing reports on how companies rate in their carbon footprint. However, the source of positive change is broader and deeper. The fundamental economic model that governs the thinking about the economy and the environment has been rapidly evolving. No longer is strong economic growth and environmental stewardship seen as being an unfortunate tradeoff. Resource efficiency is not only good for the environment, but also ultimately for companies’ earnings. As a result, there is now a consensus that environmental soundness is fully consistent with business soundness.

Lean Means Green

Lean manufacturing can be a key driver of the win-win relationship between profits and positive environmental outcomes. The ultimate goal of a lean journey is to merge quality with speed and low costs. One way in which this happens is a change in the operation of the supply chain. In the lean model, forecasted customer demands yield more responsive and more precise order delivery systems. By operating in the lean environment with its higher efficiency and greater emphasis on cost-cutting, U.S. manufacturers are positively impacting their bottom line. At the same time, lean companies are cutting down on raw material consumption, energy usage, waste, and pollution.

Measuring Company Environmental Results: The Carbon Footprint

The measurement of both environmental investments and environmental outcomes for an individual company remains a young science. Thus far, the carbon footprint remains the gold standard for gauging progress on the company level. Even carbon remains a difficult problem. The carbon footprint of manufactured products goes well beyond carbon emissions and consumption.xii It must also take into account the embodied carbon within the product. Thus, there needs to be a carbon output metric that aggregates carbon through the life cycle.

While firm answers have yet to appear on the carbon life cycle measurement challenge, there is anecdotal evidence of market-leading companies and key manufacturing industries thinking in a holistic sense about carbon emissions. A 2015 Fortune Magazine article, for example, discussed the efforts of Siemens, the automation giant. xiii Siemens planned to spend $110 million to reduce carbon emissions. The company’s goal is to cut its emissions in half by 2020 and to become carbon neutral by 2030. As one way of achieving such a challenging goal, Siemens has invested in more energy efficient manufacturing technologies. Dell, another company that is making a focused effort with its carbon footprint, is using information technology, such as big data and analytics, to reduce energy consumption in the manufacturing process.

European nations have demonstrated that the public sector can play a constructive role in carbon emissions reduction if it works within a framework that recognizes the growing tendency of markets to support environmental progress. In 2012, for example, the European Commission set targets for manufacturers of new cars and light commercial vehicles to reduce carbon emissions. Fines were enforced for non-compliance, but there were also productive innovation incentives. The EU incentivized member states to introduce measures to encourage consumers to purchase more fuel-efficient cars.

Sources: U.S. Bureau of Economic Analysis and MAPI Foundation

Measuring Aggregate Results: Encouraging Signs

Encouraging evidence points to positive results from changes in corporate environmental behavior. A 2015 study from the National Bureau of Economic Research notes that between 1990 and 2008 air pollution emissions from U.S. manufacturing fell by 60% despite a substantial increase in U.S. manufacturing output.xiv

More recent data from the Organization for Economic Cooperation and Development (OECD) validate a positive trend. With market incentives aligned with positive environmental outcomes, the most logical forecast is for continued environmental improvement over the long-term.

This report is made possible by our underwriters:

SOURCES

i Daniel Meckstroth, The Manufacturing Value Chain is Much Bigger Than You Think, MAPI Foundation Policy Analysis, PA-165, February 2016.

ii MAPI. “China Solidifies Its Position as the World’s Largest Manufacturer.” March 30, 2015.

iii Daniel Meckstroth, The Manufacturing Value Chain is Much Bigger Than You Think, MAPI Foundation Policy Analysis, PA-165, February 2016.

iv McKinsey & Company, Manufacturing the Future: The Next Era of Global Growth and Innovation, November 2012.

v MAPI Foundation and Deloitte, Footprint 2020, Expansion and Optimization Approaches for U.S. Manufacturers, October 2015.

vi Deloitte and The Manufacturing Institute, Overwhelming Support: U.S. Public Opinions on the Manufacturing Industry, 2014.

vii U.S. Department of Labor, Bureau of Labor Statistics, Job Openings and Labor Turnover Survey.

viii U.S. Department of Labor, Bureau of Labor Statistics, Table 5. Median years of tenure with current employer for employed wage and salary workers by industry, selected years, 2006-16.

ix U.S. Department of Labor, Bureau of Labor Statistics, Employer Costs for Employee Compensation Archived News Releases.

x U.S. Department of Labor, Bureau of Labor Statistics, Occupational Employment Statistics, May 2016.

xi United States Census Bureau, Business Dynamics Statistics: Number of Firm Exits, 2014.

xii Ramon Arratia, “Galvanizing the Manufacturing Sector to Reduce Carbon Emissions,”BIU.

xiii Katie Fehrenbacher, “How Big Companies are Reducing Emissions and Making Money,” Fortune Magazine, September 29, 2015.

xiv Joshua S. Shapiro and Reed Walker, “Why is Pollution From U.S. Manufacturing Declining? The Roles of Trade, Regulation, Productivity, and Preferences,” NBER Working Paper 20879, January 2015.