Machinery and Computers Lead the Way to Stronger U.S. Manufacturing

Macroeconomic Backdrop for Total Manufacturing and Industry Subsector Forecasts

The upswing in global growth that began in earnest in the winter of 2016 continues. All told, the MAPI Foundation’s forecast remains relatively unchanged from the February 2017 report. Between 2017-2020, we expect annual U.S. GDP growth to average 2.2% and U.S. manufacturing growth to average 1.6% over the three-year period.

However, today’s global uncertainties can quickly present head- or tail-winds to future U.S. growth. In addition to our quarterly scenario for U.S. manufacturing growth, the June 2017 report also explores the boundaries of plausible factory sector growth through 2020.

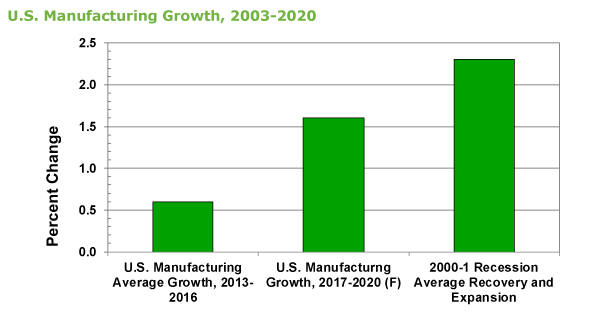

Our alternative global growth scenarios suggest a relatively narrow range for average manufacturing growth through 2020 of between 1.4% and 1.9%. Therefore, while U.S. manufacturing growth is accelerating from the weak 2013-2016 period, a return to the growth rates of the 1990s or even the early 2000s is unlikely.

Forecast of Total Manufacturing and Major Manufacturing Subsectors

MAPI Foundation’s current projections for growth in U.S. GDP, as well as key components of GDP through 2020, are based on the low likelihood of recession before 2020. Relatively low interest rates and the nonzero probability of growth-enhancing fiscal stimulus contribute to this prediction.

The four-year outlook for U.S. manufacturing growth and growth in major U.S. manufacturing subsectors is moderate. We anticipate constraint in the short term due to a range of uncertainties, including globally slow labor productivity growth. Conversely, there may be limitations over the long-term by demographic and labor supply challenges.

In a still tight global business climate, the factory sector landscape is experiencing an increasingly sharp division between the fortunes of winners and losers. Overall, stronger industry subsectors have an improved outlook while the weaker industry subsectors have a slower outlook.

Encouraging sectors:

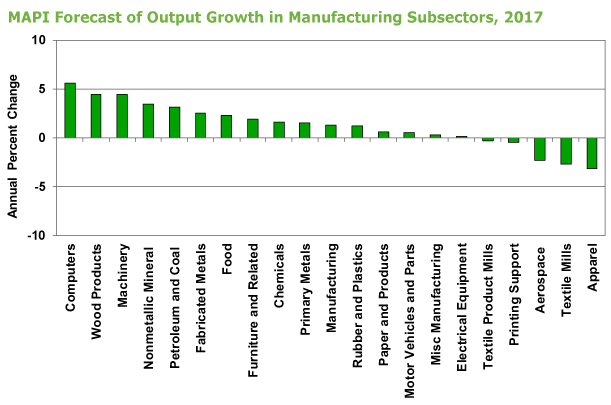

- The computer sector will be a manufacturing growth leader with an average of 4.3% growth through 2020, experiencing growth of 5.6% and 6.4% in 2017 and 2018 respectively

- The ongoing housing recovering is catalyzing wood products’ forecasted growth of 4.4% in 2017 and 3.2% in 2018

- Slowly improving global manufacturing growth brightens the outlook for the critical machinery sector that will see an average of 4.2% growth through 2020

Outlook Perspective: Consumer, Investment, and Materials-Related Industries

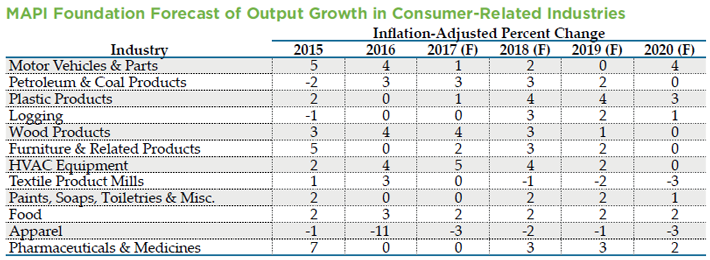

Reliable consumer spending remains the chief source of U.S. economic growth and consumers catalyze growth in most consumer-related industries. The two exceptions are textile product mills and apparel, both of which are industry subsectors in long-term decline.

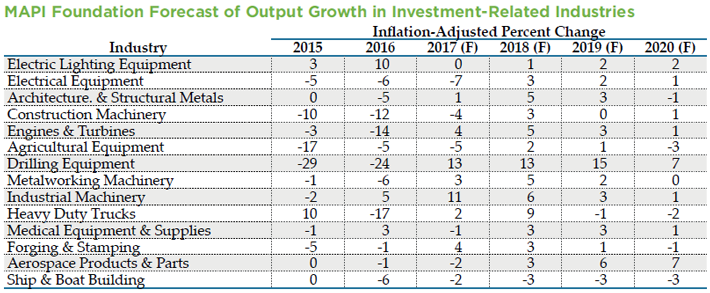

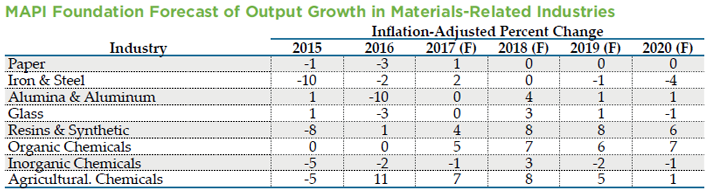

By contrast, a long-standing weakness in capital goods investment continues to contribute to volatility and weakness in investment-related industries. Lately, the outlook for the industrial machinery subsector is brighter. Two factors drive this change—an overall improvement in U.S. manufacturing growth and relatively stable energy prices that encourage drilling equipment investments. As the global economy recovers and materials prices stabilize, the outlook for growth in key materials industries has stabilized as well.

Summary

In spite of impediments from the still elevated dollar and the weak capital spending, improvement in global economic growth resulted in a positive impact on the U.S. manufacturing outlook. While our forecast predicts manufacturing growth will remain weaker than historical norms, we expect it to more than double from the feeble average rate of the 2013-2016 period.

Consumer-related industries have by far the strongest and most stable growth outlook. Long-standing weakness in capital goods investment has contributed to volatility and weakness in investment-related industries. However, the slowly improving manufacturing growth picture, both in the U.S. and globally, continues to brighten the outlook in the critical machinery and computer subsectors. Full details from the Foundation’s global growth forecast are available in the Stronger World Propelling U.S. Manufacturing report.