U.S. Industrial Outlook: Glimmers of Light

Overview of the Forecast Picture

In recent months, there have been a number of welcome signs of stability in the global economic picture. A firming of price pressures and trade flows in key regions has eased fears of a lapse into growth-destroying deflation. Economic and political turmoil appear to have reached a trough in a number of large emerging markets, most notably Brazil and Russia. Slow and slowing growth in the eurozone and China remain a concern for the global economy, but fears of a hard landing and/or imminent crisis in these two regions are receding.

We still forecast modest to moderate U.S. economic performance and relatively sluggish manufacturing output growth. We expect annual U.S. GDP growth to average 2.3% between 2017 and 2020. U.S. manufacturing output growth is expected to average only 1.5% over this period. However, we see multiple risks to both outlooks, including moderately higher interest rates, a high dollar, Brexit’s reverberations, and concerns over geopolitical tensions in the trade arena.

The harsh reality of historically slow global economic performance remains in place, and the U.S. economy and U.S. manufacturing sector continue to confront a host of performance-impeding challenges. Capital spending, a key demand driver for the U.S. factory sector, is only slightly stronger in this new forecast, still far weaker than the low double-digit growth rate that was once the norm for equipment investment growth. This longstanding problem has created an almost structural demand deficit for U.S. manufacturers. Further, weak capital spending is one factor in a sluggish productivity picture for the economy and manufacturing, with a host of implications for future growth, wages, and living standards.

While world growth might be slightly firming and strengthening, the global bias toward the dollar is unlikely to change in the next few years, as the meaningful gaps in economic growth and interest rates between the U.S. and the rest of the world are likely to remain favorable to the greenback. This is a frustrating, profit-killing problem for U.S. manufacturers that struggle for price advantage in a difficult global business environment.

Normal forecast uncertainty is growing, as political and policy uncertainty are rapidly rising as elements of the U.S. manufacturing growth outlook. The potential flow of new U.S. tax, regulatory, healthcare, and trade policies could very well add a measure of dynamism and rapid change for the short-term manufacturing growth outlook, the likes of which have not been seen in quite some time.

MAPI Foundation Forecast of U.S. Economic and Manufacturing Growth

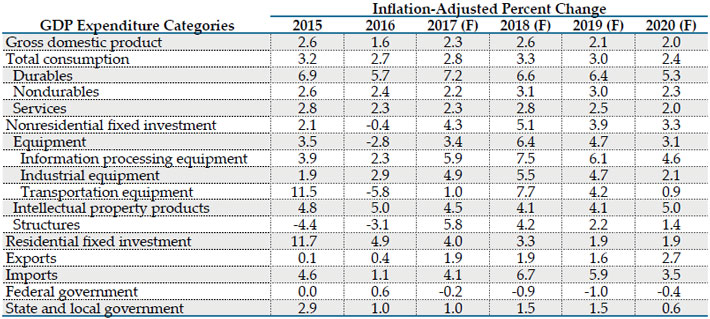

Table 1 shows the MAPI Foundation’s current predictions for growth in U.S. GDP and key components of GDP through 2020. Historically low interest rates and the likelihood of growth-enhancing fiscal policies suggest that a recession, at least a major recession, will not occur over this period.

Table 1 – MAPI Foundation Forecast of U.S. Growth of GDP and Components

F=Forecast

Source(s): MAPI Foundation, February 2017

Growth is nonetheless likely to remain moderate, extending the post-2005 period in which annual U.S. economic growth has not reached or exceeded 3%. The realities of an aging population and the uncertain path of recovery from very weak productivity performance are significantly affecting potential growth, the rate at which an economy can grow in a stable, non-inflationary manner. Nonetheless, this is an improvement from our December 2016 forecast.

As in our last forecast, we expect moderate consumer spending to be the primary growth driver. By contrast, our prediction for the growth of equipment investment remains disconcertingly slow, although the forecasted 4.4% average growth in business equipment spending over the 2017-2020 forecast period is an improvement from the 3.8% that we expected just three months ago. Even with our model-driving assumption of moderate improvement in global growth, still subpar global demand and a high dollar are expected to yield annual export growth of less than 2% until 2020, when export growth is expected to pick up very modestly to 2.7%.

With only moderate improvements in the still problematic outlook for capital spending and export demand, it is not surprising that the U.S. manufacturing growth forecast is only incrementally improved from December. As shown in Table 2, manufacturing growth is expected to be a weak 1.2% in 2017, accelerate to 2.6% in 2018, and slow rather significantly in 2019 and 2020. Average annual manufacturing output growth is expected to be 1.5% between 2017 and 2020, slightly better than the 1% average seen in our December 2016 forecast.

Table 2 – MAPI Foundation Forecast of U.S. Manufacturing Output Growth

F=Forecast

Source(s): MAPI Foundation, February 2017

Forecasts of Major Manufacturing Industries

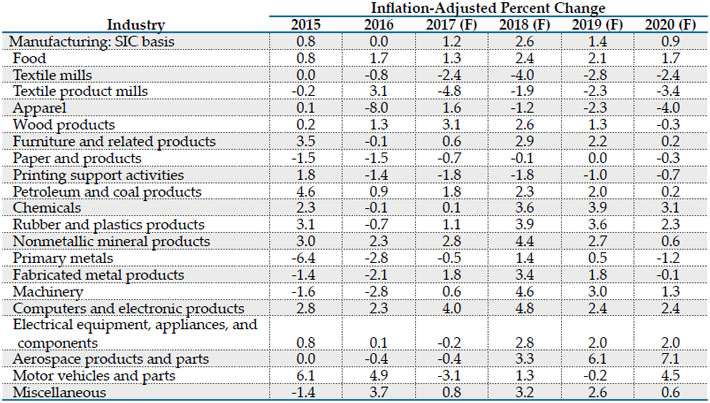

Table 3 shows the four-year outlook for major U.S. manufacturing industries. Amidst a generally sluggish picture, food, chemicals, and aerospace are the industries with relatively strong growth outlooks through 2020. There is a modest improvement in the machinery outlook when compared with our December 2016 simulation. This is likely driven by a slightly stronger capital spending prediction. The computer industry output forecast has strengthened as well, the predictable consequence of a modestly stronger economic growth scenario.

Table 3 – MAPI Foundation Forecast of U.S. Manufacturing Industry Output Growth

F=Forecast

Source(s): MAPI Foundation, February 2017

Miscellaneous manufacturing has a relatively strong outlook. This subsector includes medical equipment, a growth industry that is increasingly benefiting from an aging population, as well as some specialized consumer products such as sports equipment that benefit from the generally positive tone of consumer spending.

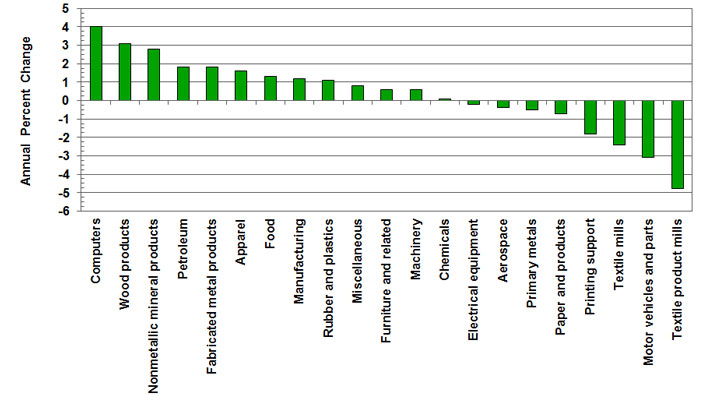

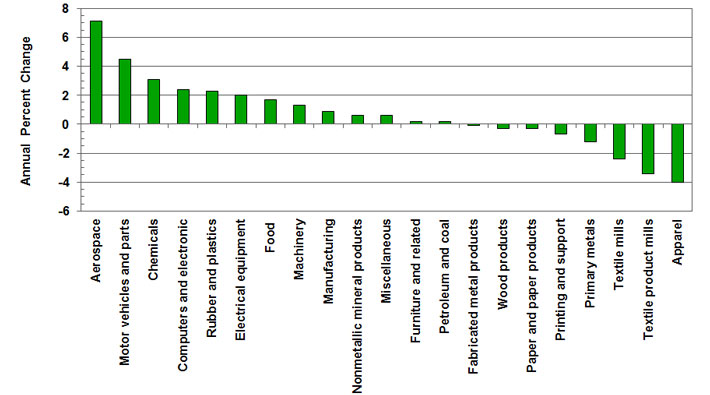

Figures 1 and 2 show the lineup of our industry output growth forecasts for 2017 and 2020, the first and last years of the forecast period. While computers and wood products are among the strong performers in 2017, aerospace and motor vehicles are predicted to be the dominant growth industries in 2020.

Machinery moves up modestly in the forecast rankings from 12 in 2017 to 8 in 2020. The machinery forecast could be even more dynamic if the growth outlook continues to improve and if new fiscal policies effectively target equipment investment. However, higher interest rates and a stubbornly strong dollar present risks to machinery demand.

Figure 1 – MAPI Foundation Forecast of Output Growth in Manufacturing Industries, 2017

Source(s): MAPI Foundation, February 2017

Source(s): MAPI Foundation, February 2017

Outlook Perspective: Consumer-, Investment-, and Materials-Related Industries

For further perspective, Tables 4, 5, and 6 segment detailed industry forecasts into consumer-, investment-, and materials-related manufacturing, respectively.

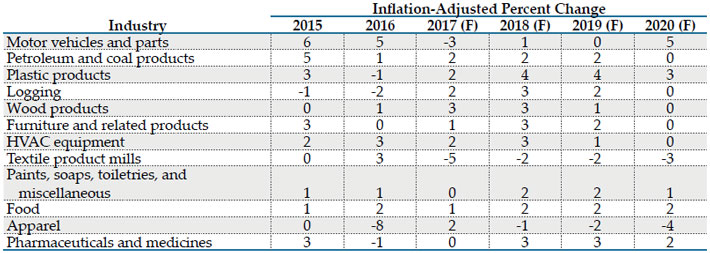

Table 4 – MAPI Foundation Forecast of Output Growth in Consumer-Related Industries

F=Forecast

Source(s): MAPI Foundation, February 2017

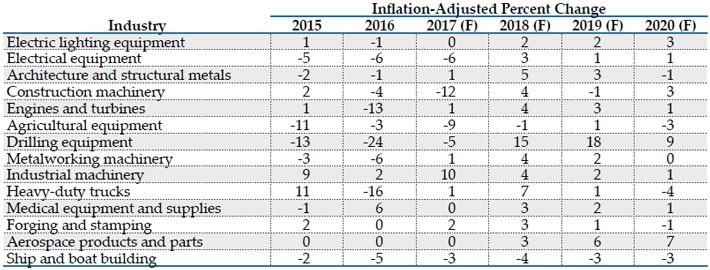

Table 5 – MAPI Foundation Forecast of Output Growth in Investment-Related Industries

F=Forecast

Source(s): MAPI Foundation, February 2017

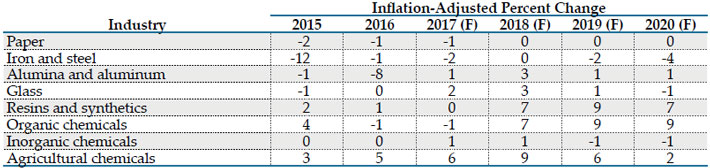

Table 6 – MAPI Foundation Forecast of Output Growth in Materials-Related Industries

F=Forecast

Source(s): MAPI Foundation, February 2017

Apart from textile product mills and apparel—both industries in long-term decline in the U.S.—the consumer-related manufacturing growth outlook is generally positive, if not strong, reflecting our forecast of moderate and steady consumer spending.

While investment-related manufacturing has the weaker and more volatile outlook, there has been some strengthening in the industrial machinery forecast. Expected volatility in drilling equipment output is partially a response to what has been a dramatic oil price cycle.

Materials production forecasts reflect the expectation of some stabilization in the global economy. The iron and steel outlook, while somewhat improved, reflects steel gluts and the still slow U.S. manufacturing outlook.

Forecast Issues and Risks

Forecast risks have not changed markedly since the publication of our December 2016 industrial outlook, although an upside surprise on near-term global growth and thus on U.S. manufacturing growth has emerged as a slight possibility.

Otherwise, we continue to watch for the possibility that the new U.S. Congress will soon enact tax and regulatory reform and pass a significant infrastructure spending bill. Such measures add a positive risk to both the U.S. and global growth outlooks.

Counterbalancing these positive risks are the impact of Brexit as it shapes UK and eurozone growth and the potential for upside risks on the outlook for U.S. and global interest rates. As we noted in our December report, upside surprises in interest rates and the dollar could somewhat neutralize the positive impacts of new growth-enhancing policies in the U.S.

Looking Ahead

While our U.S. GDP and manufacturing forecast is only modestly stronger than our December simulation, a multitude of turning points will shape the MAPI Foundation forecast in the quarters to come.

A possible firming of global growth and the prospect of new growth-enhancing policies in the U.S. place a positive spin on the forecast, while moderately higher interest rates, a high dollar, and concerns over geopolitical tensions in the trade arena are all concerns for the U.S. growth and manufacturing outlook.