Aerospace, Capital Goods, and Chemicals Propel U.S. Manufacturing

Macroeconomic Backdrop for Total Manufacturing and Industry Subsector Forecasts

The acceleration in global economic growth that began in late 2016 looks increasingly sustainable. A marked improved in economic activity is becoming apparent in regions that matter to U.S. manufacturing prospects, including East Asia, the Eurozone, and Canada. In spite of two devastating hurricanes, U.S. economic growth has averaged 3.1% in the second and third quarters of 2017, up from a 2% average over the prior four quarters. Unless the recent growth improvement in the U.S. is fleeting, it adds a further significant upside prospect for world economic performance.

There are potential downside influences as well, many of which come from outside of the economic sphere. Political and policy concerns in Washington and London, nuclear tensions with North Korea and Iran, and the growing threat of protectionist policies in North America all lend a tone of uncertainty to the global picture. Risks aside, the MAPI Foundation’s projection for U.S. economic growth remains almost completely unchanged from our June and September reports. Between 2017 and 2021, we expect annual U.S. GDP growth to be an average of 2.1%.

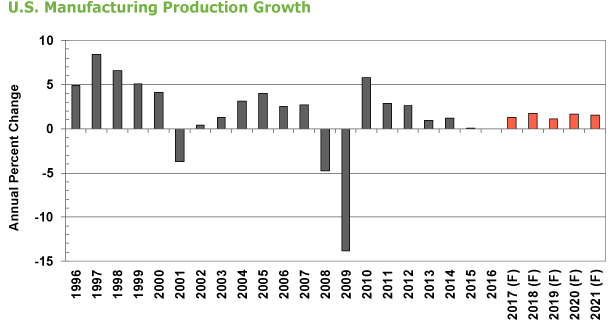

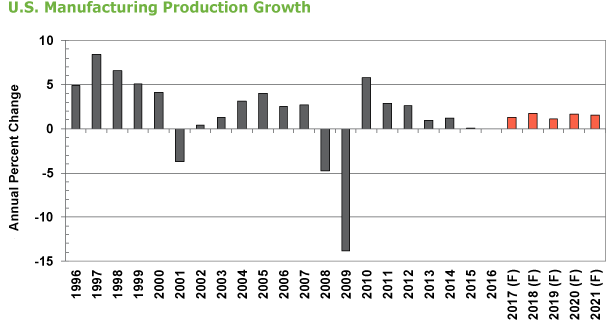

U.S. manufacturing performance is tied to a world picture that is often volatile and increasingly integrated along both economic and political dimensions. To provide a broader scope, the Foundation simulates a number of global growth scenarios. Currently, such analysis suggests a range for average U.S. manufacturing growth through 2021 between 1.2% and 1.8%. While certainly an improvement from the near stagnation of the 2013-2016 period, this will be historically weak performance.

F=forecast; Sources: Federal Reserve Board and MAPI Foundation, November 2017

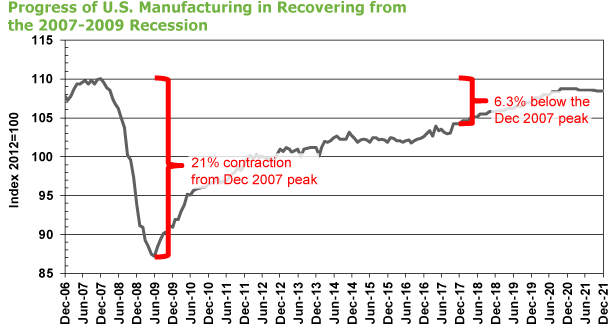

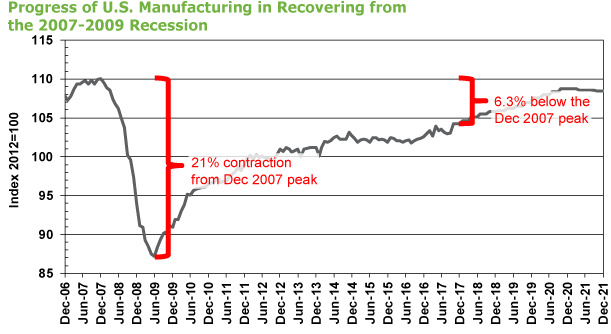

In testimony to the struggles of recent years, the U.S. manufacturing sector has yet to fully recover from the Great Recession during which it suffered from a 21% contraction from the pre-recession peak, reached in December 2007. The MAPI Foundation has been tracking the progress of U.S. manufacturing in regaining the output that was lost during the deep and destabilizing 2007-2009 downturn. As of September 2017, output remains 6.3% below the December 2007 level. Under our current projections for manufacturing output growth, the factory sector will fall short of regaining its lost output even by the end of 2021.

Sources: Federal Reserve Board and MAPI Foundation, November 2017

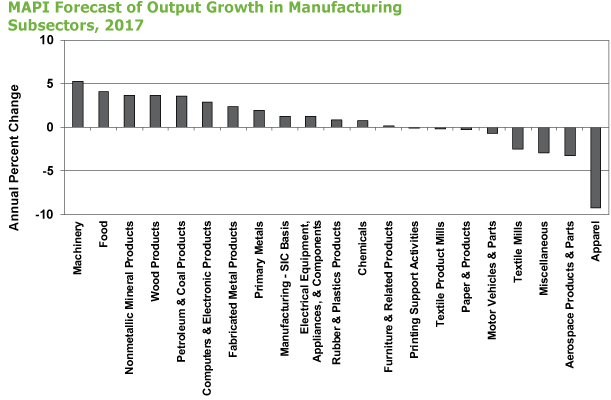

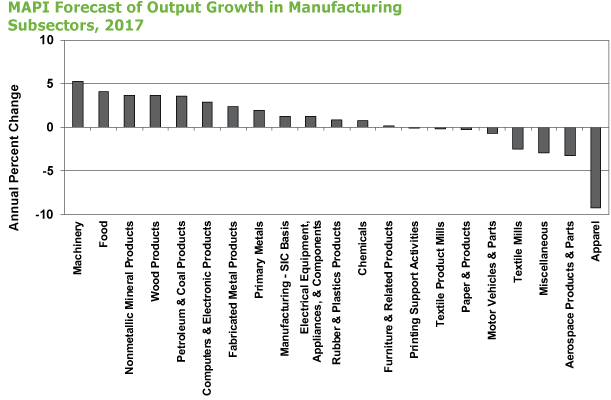

Forecast of Total Manufacturing and Major Manufacturing Subsectors

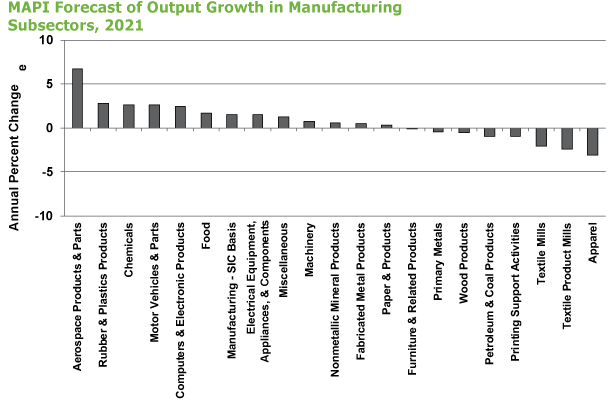

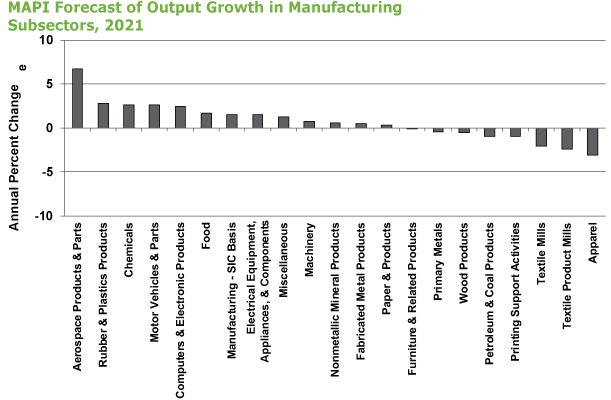

Beginning with this report, we extend our industry subsector forecasts to 2021. In the previous 2017 reports, the forecast period extended to 2020.

The outlook for U.S. manufacturing growth and growth in major subsectors paints a picture of both improvement and struggle. At the moment, the factory sector is overly reliant on a small number of subsectors for forward momentum. As such, there is a wide divergence between the prospects for strong industries and weak industries. Weak industries are suffering under the weight of a complex picture of structural change in everything from workforce-related demographics to technological disruption.

Textile mills, textile product mills, and apparel all have especially bleak outlooks. We project a 4.5% average decline in apparel output through 2021. Textile mills and textile product mills are not faring much better with the expectation of a 2.6% average decline and a 1.9% average decline, respectively. These numbers may not reveal the full picture. As has been the case in other sectors such as agriculture, contraction and bleak outlooks can mask structural dynamism. The forecast could change if these industries were to reverse course as a result of a reshoring wave that would be partially motivated by the prospects of a more automated, cost-constrained production environment augmenting the advantages of a domestic U.S. supply chain. Nonetheless, it is clear that overall U.S. manufacturing growth, productivity, and competitiveness are going to be increasingly dependent upon the success of export prowess in the innovation-intensive durable goods industries, with a notable focus on capital equipment for production.

Source: MAPI Foundation, November 2017

Encouraging subsectors:

- The computer and electronic products subsector and the machinery subsector are benefitting from a global economic recovery and a modest manufacturing rebound. The annual growth of machinery subsector output is expected to average 2.5% through 2021, while the average growth of computers and electronic products output is projected to be just a bit stronger at 2.6%. If the recent strengthening of U.S. equipment spending growth foreshadows a stronger period of U.S. business investment, then the outlook for these two sectors will strengthen.

- After an expected 3.3% output contraction in 2017, the aerospace products and parts subsector is projected to enjoy a strong 3.8% average growth rate through 2021. Improved global performance and the resumption of strong demand for air travel are tailwinds propelling this high-flying industry area, one of the most globally competitive in U.S. manufacturing. Currently, the strength in aerospace is coming from the commercial sector. Inflation-adjusted U.S. federal government expenditures on defense spending contracted between 2011 and 2016. As geopolitical pressures mount for increasing defense spending, however, this could stimulate the national security section of the aerospace market and thus create an even stronger outlook.

- While the recent hurricanes lowered projected output growth in the chemicals subsector for 2017, the average growth forecast through 2021 is a solid 2.6%. The ongoing U.S. housing recovery, moderate but steady consumer spending, and demographic tailwinds for the pharmaceuticals industry are all making chemicals a solid performer.

Source: MAPI Foundation, November 2017

Outlook Perspective: Consumer, Investment, and Materials-Related Industries

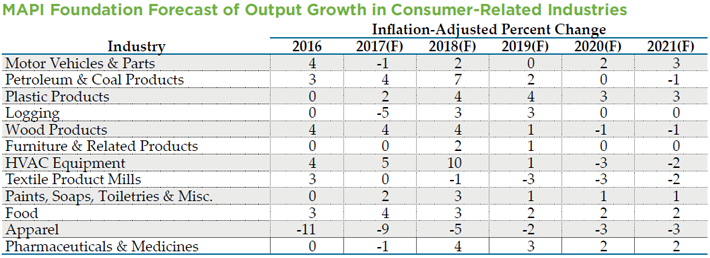

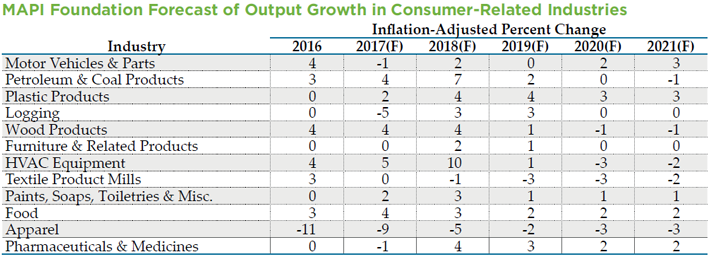

As the U.S. housing rebound matures and as job growth is projected to slow, signs of modest weakening in the outlook for consumer-related industries growth begin to appear. While wood products output is projected to be a moderately strong 4% for 2017 and 2018, its growth projection then flattens for the balance of the forecast period through 2021. After 2018, the furniture output forecast also becomes sluggish. Apparel and textile product mills are troubled subsectors who have yet to show evidence of a bottom in their persistent output decline.

F=forecast; Source: MAPI Foundation, November 2017

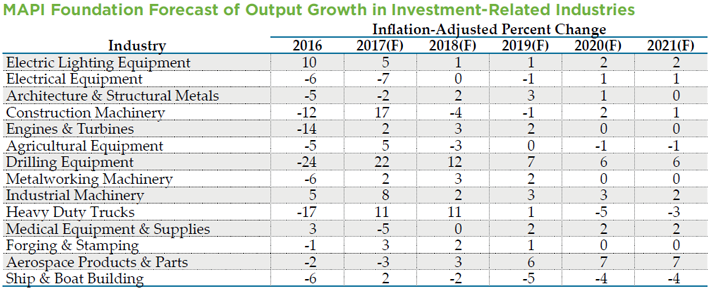

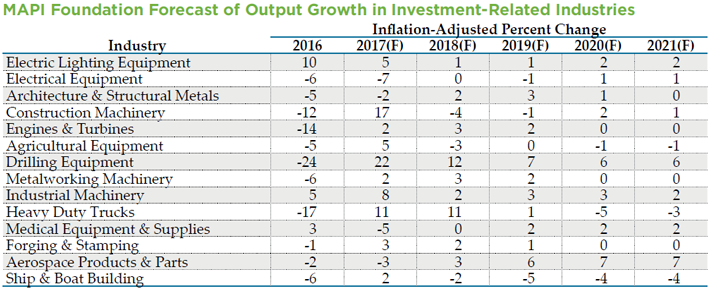

Industrial machinery, metalworking machinery, electric lighting equipment, and aerospace are among those with the steadier outlooks in the investment-related industries group. These are catalyzed by a durable housing recovery and an improving manufacturing sector. The expected steadiness in oil prices is certainly a boon for the drilling equipment outlook, which is expected to remain strong for the balance of the forecast period.

F=forecast; Source: MAPI Foundation, November 2017

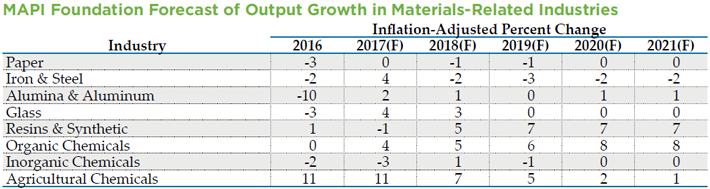

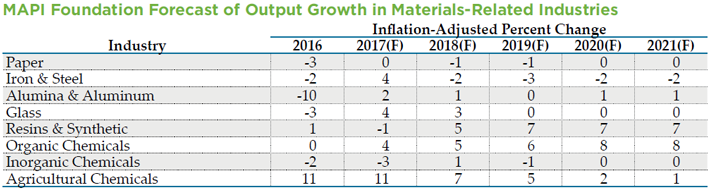

Even outside of the residual effects of the politically sensitive global steel glut that was widely discussed at the G20 Summit, the growth outlook for materials-related industries is variable. A rebounding global economy has steadied performance in these industries. But there are industry-specific issues related to the globalization of production and regulation.

F=forecast; Source: MAPI Foundation, November 2017

Summary

Aerospace, machinery, computers, and chemicals are the four subsectors that are most responsible for catalyzing the modest forward momentum in U.S. manufacturing growth. The outlook for consumer-related industry growth is showing some weakening particularly in wood, furniture, and HVAC equipment as the housing recovery matures and as job growth slows. Investment-related industries that are tied to the manufacturing rebound, such as industrial machinery and metalworking machinery, have the steadiest outlooks through 2021. Full details of the Foundation’s U.S. economic growth forecast are available in Moderate Manufacturing Outlook Amidst an Improving Global Picture.