The Impact of Hurricane Harvey on the U.S. Manufacturing Outlook

By Cliff Waldman, Chief Economist

By now, the staggering physical impact of Hurricane Harvey, with its overwhelming 52 inches of rain, is well known. There are 58 counties in Texas alone that have been declared disaster areas and are thus eligible for federal disaster assistance. Tragically, there are more than 60 deaths known thus far. Houston is the fourth most populated city in the U.S., so U.S. housing stock as a whole is significantly affected. While estimates vary, NPR quoted the White House on September 1 stating that 100,000 homes were impacted by the storm.

As the flood waters recede and the long rebuilding process begins, it is important to assess the impact on the U.S. economy and the U.S. manufacturing sector. Policymakers need to minimize the downstream negative impacts from an already destructive event. Manufacturing executives need to readjust their business plans to account for a significant disruption. Analysts who are bravely offering early estimates are projecting that Harvey will shave between 0.1 and 0.5 percentage points off of third quarter 2017 U.S. GDP growth, with a modest boost to growth in the fourth quarter of 2017 and early 2018. The general pattern of a moderate hit to growth followed by a modest rebound is consistent with historical experience. Nonetheless, with an event of this almost unprecedented magnitude, there is room for error, including either an underestimate or an overestimate of the policy response in these politically divisive times.

Proportionately speaking, the impact of Harvey on the manufacturing sector will likely be larger than for the U.S. economy as a whole. Manufacturing has finally been strengthening from years of stagnation. Key data points that reflect manufacturing activity just before the hurricane sent positive signals on the persistence of a moderate improvement in factory sector growth that began in early 2017 after four nearly stagnant years. The Institute for Supply Management (ISM) reported that the Purchasing Managers’ Index jumped a significant 2.5 percentage points in August to 58.8%, more than three percentage points above the 12-month average. The new orders and production indices are at remarkably strong levels, above 60%. The backlog of orders index jumped to 57.5%, indicating that there is adequate pressure on the production schedule to lend momentum to current manufacturing growth. Comments from survey respondents highlight a steady, if not booming, global business climate.

Improved factory sector activity is doing good things for the U.S. manufacturing workforce. Ninety minutes before the ISM released its latest survey data, the Bureau of Labor Statistics (BLS) revealed that U.S. manufacturing added a strong 36,000 jobs to its payrolls in August. The employment gains were widespread. Motor vehicles, fabricated metals, computers and electronic products, and food all experienced significant job additions. As BLS notes, the U.S. manufacturing sector has added 155,000 jobs since a recent employment low in November 2016.

While economic growth in the U.S. remained moderate and burdened with political and geopolitical risks, the world is finally a tailwind for U.S. factory sector fortunes. A coordinated global upturn remains on track. And the elevated dollar has been falling since January.

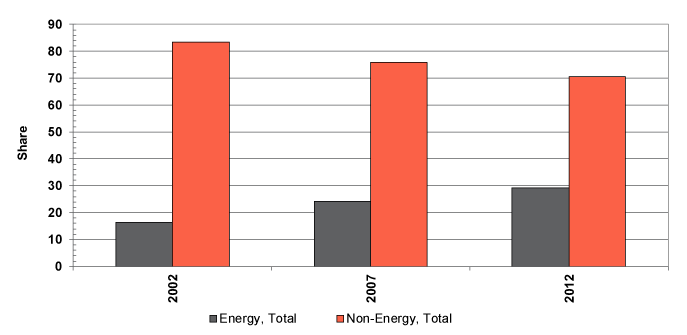

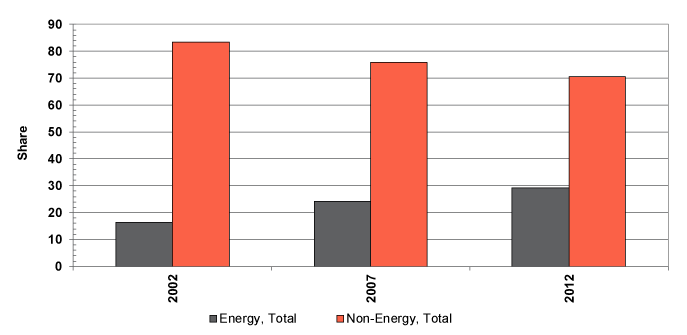

Then a consequential disaster struck. The hurricane descended upon an oil and chemical epicenter at a time when energy is growing in importance to manufacturing. Between 2007 and 2012, the share of energy output in total U.S. industrial output grew from 16.4% to 29.3%. Supply disruptions will lead to key raw material price distortions and supply chain issues. From August 21, four days before the storm hit the Southeast Texas coastline, and the latest reading on September 4, regular conventional average U.S. retail gasoline prices rose from $2.27 per gallon to $2.64 per gallon, the highest in two years.

Energy and Non-Energy Output Share of Total U.S. Industrial Output

Source: Federal Reserve Board

The factors that will matter to the manufacturing impact of the storm are clear. The degree and duration of raw material supply disruptions and price distortions are now a critical outlook issue. Also, supply chain disruptions arising from factory infrastructure damage and post-storm transportation challenges might very well make it more difficult for some manufacturing industry segments to recover. On the positive side, once the rebuilding of the housing stock begins in earnest it could be a powerful growth stimulant for U.S. manufacturing.

In these days immediately following this tragic 1,000-year flood, there are too many uncertainties for a model-based, quantitative assessment of the impact of the hurricane on the manufacturing growth outlook. The global forces that have been strengthening manufacturing and leading the factory sector into better times are unlikely to be derailed even by this harsh weather disaster. However, the disruptions to key inputs of manufacturing production and supply chain functioning could make Harvey more than just a blip for manufacturing growth. Conversely, the rebound, when it does come, might join a growing number of tailwinds for U.S. industry. Upcoming data reports, particularly the ISM manufacturing report for September, will add much-needed clarity. The MAPI Foundation will be monitoring events and data releases and will be conducting further analysis as warranted.